Dollar-Cost Averaging: The Stress-Free Strategy Smart Investors Use

Discover how dollar-cost averaging takes the guesswork out of investing. Learn why DCA beats emotional decisions, with real numbers on S&P 500 performance and Bitcoin DCA examples.

Dollar-Cost Averaging: The Stress-Free Strategy Smart Investors Use

Imagine if every time the stock market dipped, someone handed you a form to sign that said: "I promise to buy more stocks at lower prices." Most investors would jump at the chance. Yet that's essentially what dollar-cost averaging does—automatically, without you lifting a finger.

DCA isn't complicated. You invest a fixed amount of money at regular intervals—say $300 every month—regardless of whether prices are up or down. When markets crash, your $300 buys more shares. When markets soar, it buys fewer. Over time, your average cost smooths out, and you avoid the twin killers of investing: fear and greed.

Why Timing the Market Is a Fantasy

The investment world has a brutal saying: "Time in the market beats timing the market." Every major study confirms it. The problem is that human brains are wired to panic at the worst moments. When markets drop 20%, fear tells you to sell. When they rise 30%, greed tells you to pile in. Both moves are exactly wrong.

DCA solves this mechanically. You pre-commit to a schedule and let the algorithm handle the rest. A Vanguard study found that investors who made regular contributions to their 401(k) over 10 years outperformed those who tried to time the market by an average of 1.5% annually. That might sound small, but over decades, it's the difference between retiring at 65 and working until 70.

Here's a simple example: Say you invested $1,000 monthly into the S&P 500 from March 2000 through December 2005—covering the dot-com crash and recovery. That investor accumulated roughly 28% returns. Meanwhile, money market funds were yielding 0.23%. The discipline of continuing to buy through a catastrophe paid off handsomely.

The Numbers Don't Lie: DCA vs. Panic

Let's make this concrete with a scenario that actually happened.

In January 2009, the S&P 500 had crashed roughly 57% from its 2007 peak. Anyone who pulled their money out locked in catastrophic losses. But an investor who kept investing $1,000 per month throughout 2008 and 2009? Their consistency paid off as markets recovered.

By contrast, imagine someone who waited for the "perfect" entry point. They sat in cash for 18 months, missed dividends, and ultimately bought right before another dip in 2011. Research from Dalbar shows the average equity fund investor earned just 4.1% annually over 20 years while the S&P 500 returned 10.8%. The gap? Emotional decisions.

DCA doesn't make you immune to volatility, but it dramatically reduces the temptation to make things worse by selling low.

Where DCA Really Shines: Volatile Assets

Here's where dollar-cost averaging becomes especially powerful: cryptocurrencies.

Bitcoin swings 10-15% in a single week regularly. Trying to "buy the dip" in crypto is like trying to catch a falling knife while wearing oven mitts. But a $50 weekly DCA into Bitcoin since 2020 would have accumulated more BTC during the 2022 crash than any human could have bought manually—because you kept buying automatically while everyone else was panicking.

Most major crypto exchanges now offer automated DCA options specifically for this reason. Binance, Coinbase, and Kraken all let you set recurring purchases. It's one of the few fintech features that genuinely helps users rather than just increasing trading volume.

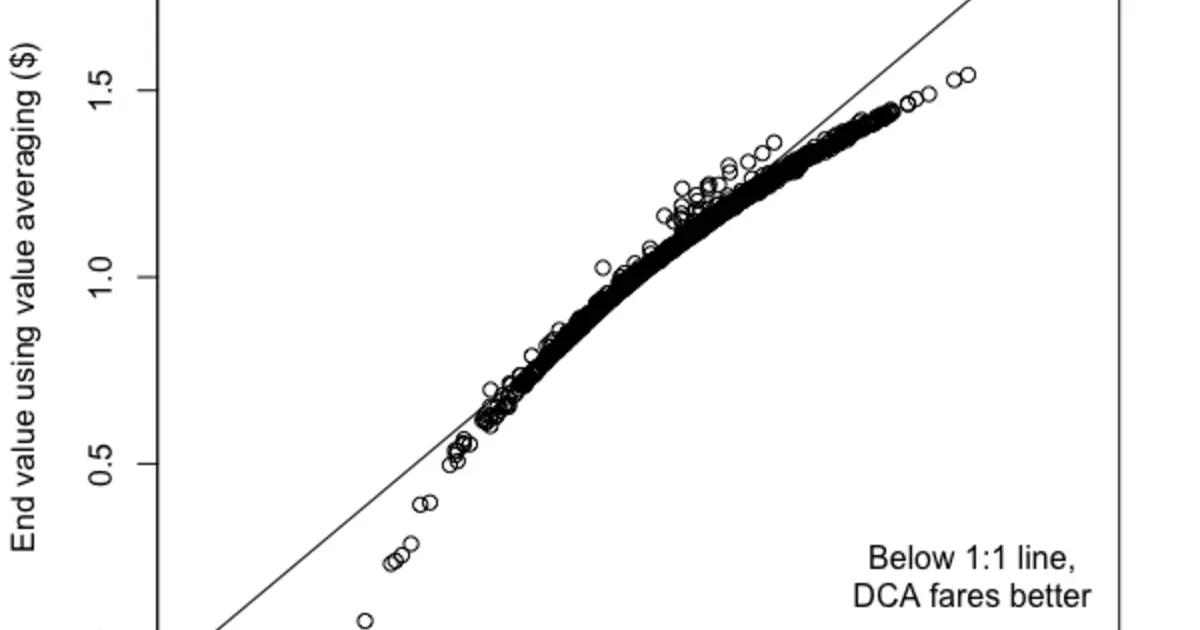

The Honest Drawbacks: When DCA Costs You Money

DCA isn't magic. In strong bull markets, it genuinely underperforms lump-sum investing. That $100,000 placed in the S&P 500 at the start of 2009 grew to approximately $1,083,000 by end of 2025. Someone who deployed $100,000 monthly over 24 months? They ended up with roughly $892,000.

The reason is straightforward: money sitting in your account waiting to be invested doesn't earn returns. In a rising market, being slowly invested means missing the early gains. The opportunity cost is real.

There's also inflation risk for long holding schedules. If you're investing $500 monthly but it takes three months to deploy the full amount, that cash loses purchasing power. This matters more in high-inflation environments—say 5%+ annually—where waiting costs you real money.

Finally, transaction costs can nibble away at small DCA portfolios. If you're investing $50 monthly and paying $5 per trade, that's a 10% fee dragging on your returns. Use commission-free platforms if you're running a DCA strategy with smaller amounts.

Practical Steps to Start DCA Today

Starting DCA requires exactly three things: a fixed amount, a regular schedule, and a platform that supports automation.

First, decide how much you can invest without straining your budget. A good rule: invest 10-20% of your monthly income consistently. Starting with whatever you can afford matters more than the amount.

Second, pick your vehicles. For beginners, low-cost index funds like the S&P 500 trackers (VOO, SPY) are the textbook recommendation. For crypto, Bitcoin and Ethereum DCA via major exchanges covers the basics.

Third, set up automatic transfers. This is the crucial step. Treat it like a bill you have to pay. If you have to manually execute the purchase every month, you'll eventually skip it.

Fourth, commit to at least 3-5 years. DCA is a long-term strategy. Short timeframes expose you to market volatility without giving the smoothing effect time to work.

The Bottom Line

Dollar-cost averaging won't make you rich overnight. It won't perfectly time the bottom of any crash. What it will do is remove the two biggest investing mistakes—buying in a panic and sitting in cash waiting for certainty that never comes.

The investors who built real wealth through 2008, through COVID, through every crash, were the ones who kept putting money to work. DCA is the system that makes that possible without requiring superhuman discipline.

Start small. Start now. Automate it. That's the entire secret.

Related Concepts:

- Lump-Sum Investing — Putting all available capital into the market at once. Outperforms DCA in rising markets but requires perfect timing.

- Volatility — How much an asset's price swings. DCA is particularly valuable for high-volatility assets like Bitcoin.

- Index Funds — Low-cost funds that track a market index. The classic DCA vehicle for beginners.

- Compound Growth — The snowball effect of reinvesting returns. DCA benefits compound growth because you're always invested.